Okay, maybe the title’s play on the famous line from John Huston’s “Treasure of the Sierra Madre” was click bait, but hey – you clicked, didn’t you? Anyway, in Europa Eyewear v. Kaizen Advisors, (D. Mass; 7/19), a Massachusetts federal court recently held that a non-signatory deal jumper was bound by a California choice of forum clause contained in the merger agreement negotiated by the two original parties to the deal.

The Court cited extensive precedent holding that a non-party may be bound by a forum selection clause if it is “closely related to the dispute such that it becomes foreseeable that it will be bound.” In this case, the jilted buyer filed a California action in which it sought damages and injunctive relief based on, among other things, the seller’s alleged contractual breaches and the deal jumper’s alleged tortious interference with that contract.

The Court ruled that since everything turned on interpretation of the underlying contract, the deal jumper’s alleged conduct was so closely related to the contractual relationship that the forum selection clause applied to it as well. The deal jumper objected on due process grounds, but the Court said that its decision to initiate the litigation by filing a declaratory judgment action was fatal to that objection:

The Court recognizes the significant due process considerations implicated where forum-selection clauses are applied to a non-signatory. In this case, however. . . Europa is the plaintiff seeking declaratory judgment not a defendant being haled into a forum with which it has no contacts. Accordingly, like all other plaintiffs, if it wishes to proceed with its claims, it must do so in the proper forum. Here, that is the Central District of California.

Check out this Ropes & Gray podcast featuring former Corp Fin Director Keith Higgins addressing the use of Rule 506(c) in the context of PE fundraising. Here’s an excerpt from an exchange between Keith & his colleague Peter Laybourn on the ability of a sponsor to flip from relying on Rule 506(b) to Rule 506(c):

Peter Laybourn: I’m sure that every fund formation lawyer out there has had instances where a client calls them up with a particular general solicitation question. I certainly know that I have had that happen multiple times.

Keith Higgins: We’ve talked about it before.

Peter Laybourn: Exactly, many times. For example, one called me up very recently and said, “Hey, we’ve just been approached by a reporter and we’d like to respond to him or her and share the details about our fund. Can we do that?” And I then have to be the bad guy and say, “No, you can’t because you’re relying on 506(b).” So Keith, do you have any advice for sponsors that find themselves in that position and who want to talk to the press?

Keith Higgins: Sure. You want to talk to the press about that specific offering and about that fund, you can flip the offering to a 506(c). In fact, unless you’ve made your first sale, you haven’t filed your Form D anyway, so you haven’t had to check the box as to whether you’re doing it under B or C, you just decide you’re going to move forward on 506(c). And the Commission staff did provide guidance that said it’s okay to flip from a B to a C – that’s good to go.

The other piece of advice on that, if you want to talk to reporters, is you have to engage in that “fencing on an electronic tightrope” where you’re talking about the general strategies of the fund complex, etc., without trying to focus in on a specific offering that you’re doing – that’s what we’ve been doing all along and it sometimes works, sometimes doesn’t. So, the surefire way to do it is to decide you’re going to do a 506(c), and particularly, if you’re selling to institutions, I think the verification shouldn’t be a big problem.

In case you’re wondering – no, I didn’t sit down & transcribe this podcast for you. But somebody at Ropes & Gray did, and the transcript accompanies the podcast. I hope other law firm podcasters are paying attention, because that’s a smart move.

A few weeks ago, I blogged about Canon & Toshiba’s unsuccessful efforts to structure an acquisition around HSR’s pre-merger notification requirements. U.S. regulators imposed a total of $5 million in monetary penalties on the parties, among other sanctions. Now European regulators have weighed in – and this Wilson Sonsini memo reports that they’ve imposed a much larger monetary sanction on one of the parties. Here’s the intro:

As the time taken to secure merger control clearances for global transactions lengthens, the parties and their advisers may be tempted to explore alternative deal structures that might allow a transaction to close sooner than otherwise expected. In a stark reminder to industry that it will not tolerate schemes that have, in its view, been devised to circumvent or undermine the efficacy of merger review, the European Commission (EC) announced on June 27, 2019 that it was fining the Japanese conglomerate, Canon, EUR 28 million (almost $32 million) for closing its acquisition of Toshiba Medical Systems (TMSC) in 2016 before notification to the EC and other competent agencies.

Like its American counterparts, the EC didn’t think the deal’s two-step structure passed muster. Instead, it viewed as a “warehousing scheme” that was part of a single transaction. Accordingly, it concluded that the transaction was subject to a notification requirement prior to the first stage of the deal, & that Canon had violated its standstill obligation by completing the first step prior to notification.

It’s been 50 years since Apollo 11, and now it looks like the prospect of space tourism is finally on the horizon. Personally, I don’t think I’m built for it. I’ve found that the harnesses on some roller coasters at Cedar Point aren’t designed for – ahem – athletic builds like mine, and I can’t imagine that I’d have better luck with whatever harness Richard Branson intends to use to strap people into their seats on his spaceship.

While I may not be in the market for a ride on a rocket, other people are excited enough about Branson’s prospects to permit his company, Virgin Galactic, to plan to go public in a deal that values the business at $1.5 billion. This Pitchbook article discusses the transaction, which will be accomplished in a very unorthodox way for such a high-profile deal – a reverse merger with a SPAC. Here’s an excerpt:

Virgin Galactic and tycoon Richard Branson are planning to take their promise of space tourism to the public markets—with a little help from Social Capital and founder Chamath Palihapitiya. A special-purpose acquisition company called Social Capital Hedosophia has agreed to purchase a stake of up to 49% in Virgin Galactic at an enterprise value of $1.5 billion, with Palihapitiya contributing $100 million and taking over as chairman of the newly combined entity. Social Capital Hedosophia will put about $800 million into the deal, according to The Wall Street Journal, a bet on Virgin Galactic’s ability to safely send earthlings into the stratosphere—and, of course, bring them back.

Reverse mergers with public shells have long been the go-to route to public status for microcaps peddling cancer cures & cold fusion. More recently, they’ve been used as a quick way to investors’ wallets by participants in the so-called “China Hustle.” While legitimate companies have successfully gone public through reverse mergers, the deal structure had been abused enough that the SEC saw fit to issue an investor bulletin on it back in 2011.

But in recent years, VCs & private equity players have entered the game and have sponsored their own SPACs. Reverse merger deals like the one Virgin Galactic & Social Capital are working on suggest that the credibility that these financial sponsors add may make this route to the public markets more attractive to real companies than it has been in the past.

Here’s an interesting new study by several prominent scholars – including SEC Commissioner Robert Jackson – that asks the question: does Revlon matter? In order to come up with an answer, the authors analyzed data from over 1,900 transactions that took place over a 15-year period. Their conclusion was that in Delaware, Revlon matters a lot – but in other jurisdictions that have adopted the standard, it doesn’t seem to move the needle. Here’s an excerpt from the abstract:

After subjecting this sample to empirical analysis, our results show that Revlon does indeed matter for companies incorporated in Delaware. We find that for Delaware Revlon deals are more intensely negotiated, involve more bidders, and result in higher transaction premiums than non-Revlon deals. However, these results do not hold for target companies incorporated in other jurisdictions that have adopted the Revlon doctrine.

Our results shed light on the implications of the current state of uncertainty surrounding Revlon and provide some direction for courts going forward. We theorize that Revlon is a monitoring standard, the effectiveness of which depends upon the judiciary’s credible commitment to intervene in biased transactions. The precise contours of the doctrine are unimportant provided the judiciary retains a substantive avenue for intervention.

In other words, the Delaware courts have demonstrated a willingness to intervene in cases of management bias that doesn’t seem to be present among courts in states where the doctrine’s been imported.

The authors note that recent Delaware decisions in C&J Energy and Corwin have been criticized for “overly restricting” Revlon, but their study suggests that those concerns are overblown so long as the transactions are monitored by Delaware judges who prioritize the substantive concerns about managerial bias that gave rise to the doctrine in the first place. They emphasize that this means not allowing the procedural emphasis of decisions like Corwin to overwhelm these substantive concerns:

Corwin, as we have already noted, focuses courts on the procedural prerequisites of a fair and fully informed vote of the disclosures under Corwin should therefore look to information that is probative of management bias, not matters that would be irrelevant to an application of enhanced scrutiny. If the plaintiffs succeed in uncovering previously undisclosed evidence of management bias, the shareholder vote should not count as “fully informed” and the cleansing effect of Corwin should not apply.

Speaking of other states, here’s a blog from Keith Bishop discussing the rather curious fact that California courts have been almost completely silent about the Revlon doctrine.

Tune in tomorrow for the webcast – “How to Handle Hostile Attacks” – to hear Goldman Sachs’ Ian Foster, Cleary Gottlieb’s Jim Langston & Innisfree’s Scott Winter provide insights into the art of responding to a hostile attack.

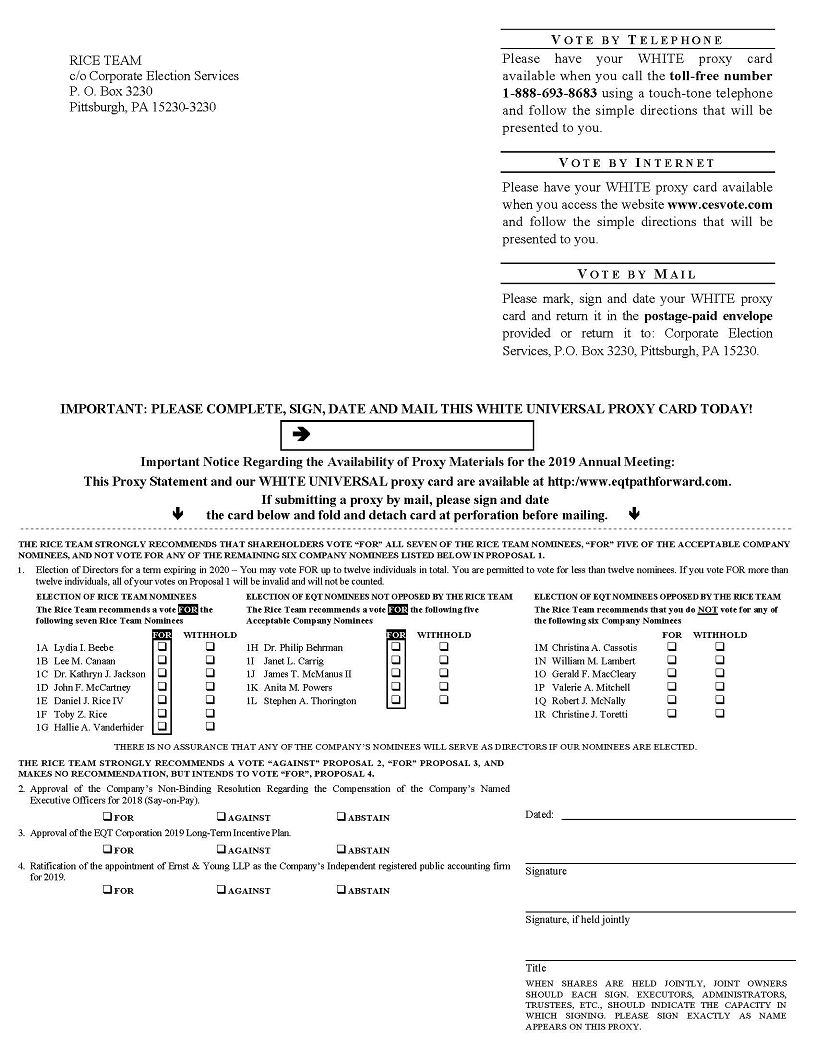

Here’s big news on the universal proxy front: yesterday, at EQT Corporation’s annual meeting, a dissident group won control of the company’s board through a proxy fight waged using a universal proxy card. According to this Olshan memo, this marks the first time that such a card was successfully used in a control proxy contest in the US. Here’s an excerpt:

The universal ballot adopted by both EQT and the Rice Team named both EQT’s and the Rice Team’s nominees on their respective proxy cards. The only difference related to the presentation of the two cards, in which each side highlighted how it desired shareholders to vote. Copies of the two cards can be found here (Rice Team) and here (EQT).

As shown, the Rice Team made clear on its proxy card a recommendation for all seven of its nominees and for five of the Company’s nominees that it did not oppose, to permit shareholders to vote for all 12 available spots. Similarly, the Company recommended a vote for all 12 of its nominees and against the Rice Team’s nominees, other than existing director, Daniel Rice IV, who was nominated by both EQT and the Rice Team.

The Rice Team obtained public support from many of EQT’s largest shareholders, including T. Rowe Price Group Inc., D.E. Shaw & Co., Kensico Capital Management Corp. and Elliott Management Corp., along with proxy advisory firms Institutional Shareholder Services (“ISS”) and Egan-Jones Ratings.

The use of a universal ballot for a majority slate of directors is unprecedented and, in our view, may become more common in future proxy contests given the Rice Team’s success here. In fact, ISS noted the following in its report recommending that shareholders vote for all of the Rice Team’s nominees on that team’s universal proxy card:

“The adoption of a universal card was an inherently positive development for EQT shareholders (as it would be in any proxy contest), in that it will allow shareholders to optimize board composition by selecting candidates from both the management and dissident slates.”

Despite pushing for the adoption of universal proxies, some activists had recently cooled on their potential use. For instance, as we blogged last fall, Starboard Value’s CEO Jeff Smith expressed concern that in its current form, the universal ballot might tip the playing field in management’s favor. It will be interesting to see if the outcome of yesterday’s EQT vote causes people to recalibrate that assessment.

Divestitures have long been used to address regulators’ antitrust concerns. Last month, the FTC’s Bureau of Competition offered up new guidance on what the agency expects from companies considering divestitures – and how to expedite the vetting process. Here’s an excerpt:

Before putting pen to paper, parties should discuss with Bureau staff what assets, rights, and personnel should be included in the divestiture package. For instance, assets outside the market of concern may be necessary for the divested business to be competitive and viable, and may need to be included in the divestiture package.

Understanding the scope of the divestiture package is a necessary prerequisite to an effective sales process, as it affects which buyers are likely to be acceptable. The acceptability of a divestiture package could vary depending on the proposed buyer. Different buyers may need more or less or different divestiture packages to be a viable competitor post-order. Proposed buyers with experience in the business – but not presently competing in the affected market – also will typically result in a shorter vetting process. Buyers with experience in adjacent geographies or complementary products or with experience selling other products to the same customer base may be good candidates. Buyers that do not have experience in the business or are purely financial purchasers will be subject to more significant scrutiny before the Bureau will be able to recommend them to the Commission.

The Bureau’s Compliance Division is experienced in vetting divestiture packages and buyers. Each divestiture order is designed to remedy the particular risk to competition created by the merger. Rather than expediting an approvable outcome, parties who skip the preliminary discussions and present signed documents may complicate staff’s analysis of the parties’ proposal and prolong, rather than shorten, the vetting process. Additionally, the Bureau may insist on revisions to the executed agreements or the scope of the proposed divestiture, and may reject the proposal completely. For this reason, it is generally much easier and more efficient to negotiate with draft documents than signed, “final” deal documents that will likely need to be modified and amended.

The FTC’s guidance notes that it has recently added resources to help guide both divesting companies and potential buyers of divested assets through the process & provide advice on what terms the FTC is likely to find acceptable in a settlement.

John Updike’s “Hub Fans Bid Kid Adieu” may be the best piece of sportswriting ever produced by somebody not named Heywood Broun, and it was the first thing that popped into my head when I was trying to figure out how to blog about Delaware Chief Justice Leo Strine’s decision to step down.

Maybe it was because like Williams, Strine was a giant in his profession for more than two decades, and like the Spendid Splinter, he was known to be somewhat prickly and notorious for not suffering fools gladly. As a result – again like Ted – Strine has both fervent admirers and rabid detractors. Both men were also never boring, and that’s saying something when one of them churned out 100+ page opinions on a regular basis.

Fortunately for you, for all the similarities that I saw between Ted Williams and Leo Strine, I found none between John Updike & myself. So I’ll make this short – whatever you may think of the guy, Chief Justice Strine has been the kind of towering presence in corporate law that Williams was on the diamond, and we’re all going to notice that he’s not on the bench.

After baseball, Ted Williams became such an expert angler that he was named to the International Game Fish Hall of Fame in 2000. We can only speculate about what’s next for Chief Justice Strine – there are already rumors of a possible run for Governor – but it wouldn’t surprise me if we end up remembering him for more than his tenure in the Delaware judiciary.

{kind=link}

{kind=link}